Parsing the productivity puzzle

09.04.17

Does the solution lie in the survival of laggard firms?

This week, when the US Bureau of Labor Statistics released data showing that productivity fell in the US in 2016, it was barely reported. Such insouciance reflects not just the difficulty of explaining its significance to a lay audience, but that the story of a productivity slowdown has become all too familiar. The general slowdown in productivity growth has become one of economics’ most widely discussed but least understood phenomena.

The facts are easy enough to state. From 1950 to 1970 median productivity growth across countries was 1.9% per year, but since 1980 it has averaged 0.3%. Productivity growth in the UK since 2008 has, on average, been negative – something that hasn’t happened for about two hundred years. This matters because long-run increases in living standards depend almost entirely on producing more with the inputs we have. Earlier this week, Christine Lagarde, of the IMF, issued a stark warning about the dire implications of continued slow growth in productivity.

Why this has happened has been the source of great head-scratching in the economics profession. Numerous explanations have been offered: that it’s harder to measure output, that it’s because we have moved into the service sector, that it’s the effect of the financial crisis, and that it’s because of low interest rates keeping dud firms alive or austerity.

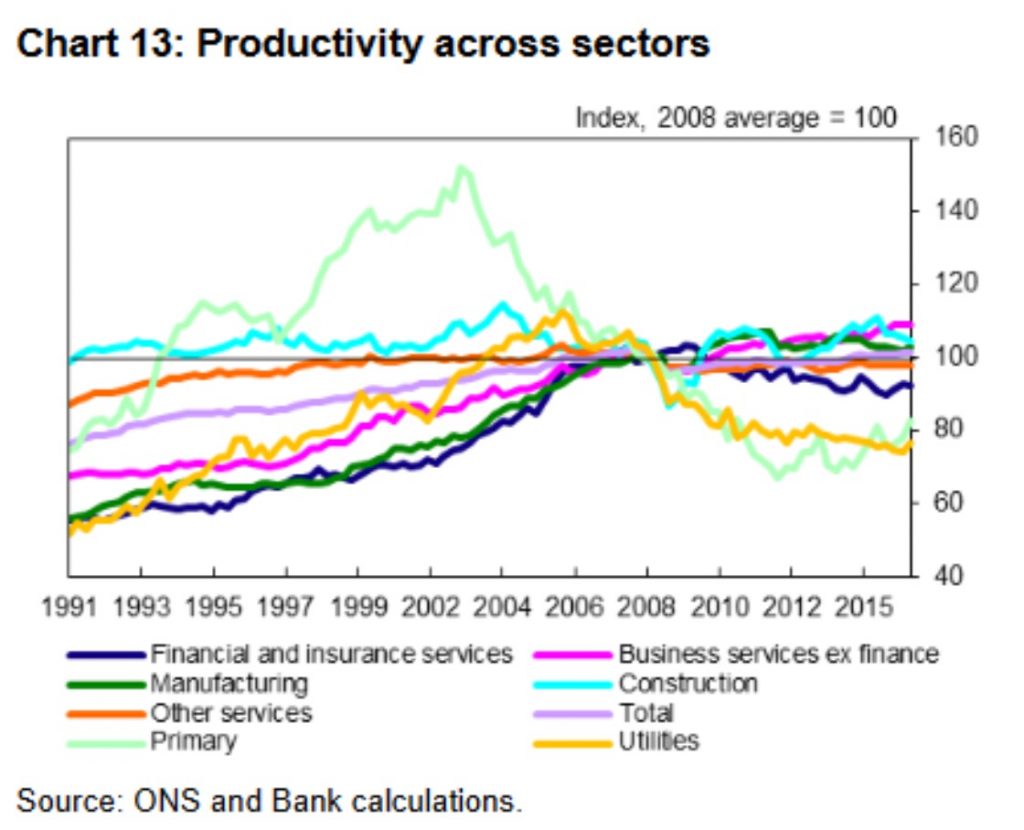

Last week Andrew Haldane, of the Bank of England, in a detailed and forensic examination of the data, became the latest to suggest a few explanations, and along the way skewered some of the more common myths. It can’t be mostly a problem of measurement, he argues, because those problems existed long before the slowdown occurred. Nor can it be because of a transition to the service sector because the slowdown has affected all sectors (see Chart). Haldane accepts that ultra-low interest rates may have kept some unproductive firms afloat, but after modelling the likely effect of higher interest rates, concludes that the effect is small.

Instead, Haldane argues that what has happened is that frontier firms (innovative firms with high productivity) have increased their productivity as rapidly or even more rapidly than in in previous eras. But those productivity gains have not spread to ‘laggard’ firms (those within the same industry, but with low productivity).

“This empirical evidence suggests a long tail of countries and companies with low, slow productivity growth. These productivity laggards have been unable to keep up, much less catch up, with frontier countries and companies….Or, put differently, rates of technological diffusion from leaders to laggards have slowed, and perhaps even stalled, recently.”

This reflects recent findings from research on innovation (discussed here). To use an analogy – if firms are runners then what has happened is that the fastest 100m runners in the world (like Usain Bolt) have been getting faster each year, but the also-rans are not making the same kind of progress. And because there are a lot of them, even though Bolt is the fastest man that has ever lived, on average runners are not much faster than they were years ago. The laggards are dragging down productivity growth – around one-third of UK firms have seen no productivity growth at all since 2000. But why, in an era of unprecedented global competition and much hype about the rapid pace of technological change, these laggards are falling ever further behind the frontier firms, remains a mystery, even to Haldane.

Haldane’s explanation hasn’t satisfied everyone. Hamish McRae still thinks it’s a measurement problem, because statisticians struggle to capture the benefits of innovations such as the iPhone. If we find new ways of measuring output, the problem might disappear:

“If you apply the Irish method of calculation to the UK, our national output has been rising just as fast after the recovery got going in 2010 as it did before 2007. The real value added in the UK economy is about £100 billion higher than estimated. That would make it about 5% bigger than currently thought.”

However, even if true this still wouldn’t explain much of the slowdown which, as Haldane points out, certainly pre-dates the iPhone.

Meanwhile, other economists have been debating the link between productivity and wages. In theory rises in labour productivity (specifically the marginal product of labour) should be the principal driver of wage increases in the long run. Indeed, Haldane finds that labour productivity can explain around 60% of the variation in average pay across firms. However a blog from Alex Tuckett, also of the Bank of England, finds a more complex relationship. The connection between wages and productivity is not straightforward and in some cases, it may be that higher wages are the cause (rather than the result) of higher productivity.

This prompted Ben Chu, of the Independent, to argue that low and stagnant wages might be the underlying cause of the productivity slowdown. And if so, then perhaps efforts to raise wages would lead to higher productivity in themselves:

“But if the chicken follows the egg, perhaps wage increases will prompt higher productivity in firms that employ low-wage labour. Perhaps, in order to protect their profit margins, managements will be spurred into increasing the efficiency of their operations. Perhaps they will invest in more capital equipment to enable their workforce to produce more per hour of their time.”

Perhaps that could explain some of the acute productivity slowdown in the UK, where real wages have fallen much further than in most other countries. But it wouldn’t help to explain the global character of the productivity slowdown, nor the fact that it has continued for decades through periods of strong and weak wage growth. The truth is that firms are continuing to operate without productivity enhancements in a variety of economic conditions.

Which brings us back to Haldane. If his thesis is true, why aren’t laggard firms – in an era of supposedly unprecedented global competition – going out of business, or alternatively being bought up by frontier firms? After all, a lower productivity growth rate would over time render the laggard firms uncompetitive, leading to lower profits. The conclusion – it seems – is that competitive pressures are much more muted than we might have expected, or else zombie businesses are being kept afloat by unusual economic conditions.

Towards the end of his speech Haldane advocated an app which could tell firms how productive they are relative to industry benchmarks. But surely the real question is why they need an app to tell them something that, in normal economic times, would be the difference between profit and bankruptcy. The last piece of the productivity jigsaw might be to work out why productivity no longer seems to matter so much to firms.

Edited by Bill Emmott

- Overall:

- Demography:

- Knowledge:

- Innovation:

- Openness:

- Resilience: